On 1 June 2026, Salesforce signed a definitive agreement to acquire Contentful, the API-first headless CMS used by more than 4,800 of the world’s leading brands to deliver digital experiences across every channel.

The irony is sitting right there in the press release, and nobody seems to want to say it: Contentful’s entire appeal was that it was not owned by a platform like Salesforce.

Why Enterprises Chose Contentful

Contentful was built on a problem that was costing enterprises real money. Traditional CMS platforms were monolithic, tying your content directly to a presentation layer, which meant a separate system for your website, your mobile app, your kiosks, and every other channel you needed to serve. The headless model solved this by decoupling content from presentation entirely, giving teams the ability to author once and publish everywhere without depending on any single vendor’s front-end decisions.

That structural independence is why Contentful became the default. By its own announcement of the deal, it was handling 180 billion API calls a month, double its 2023 volume, with an ecosystem of more than 20,000 apps and integrations, and it earned trust precisely because it played well with everything and answered to nobody.

What Salesforce Actually Bought

Salesforce needed a content engine for its Headless 360 initiative, one that was API-first and composable, and Contentful fits the brief exactly. Agentforce, Salesforce’s AI agent platform, needs to query, assemble, and deliver content dynamically, and a native structured content layer makes that meaningfully more capable.

The strategic fit is real, but the lens through which Contentful customers need to read this deal is not the product announcement, it is the acquisition history.

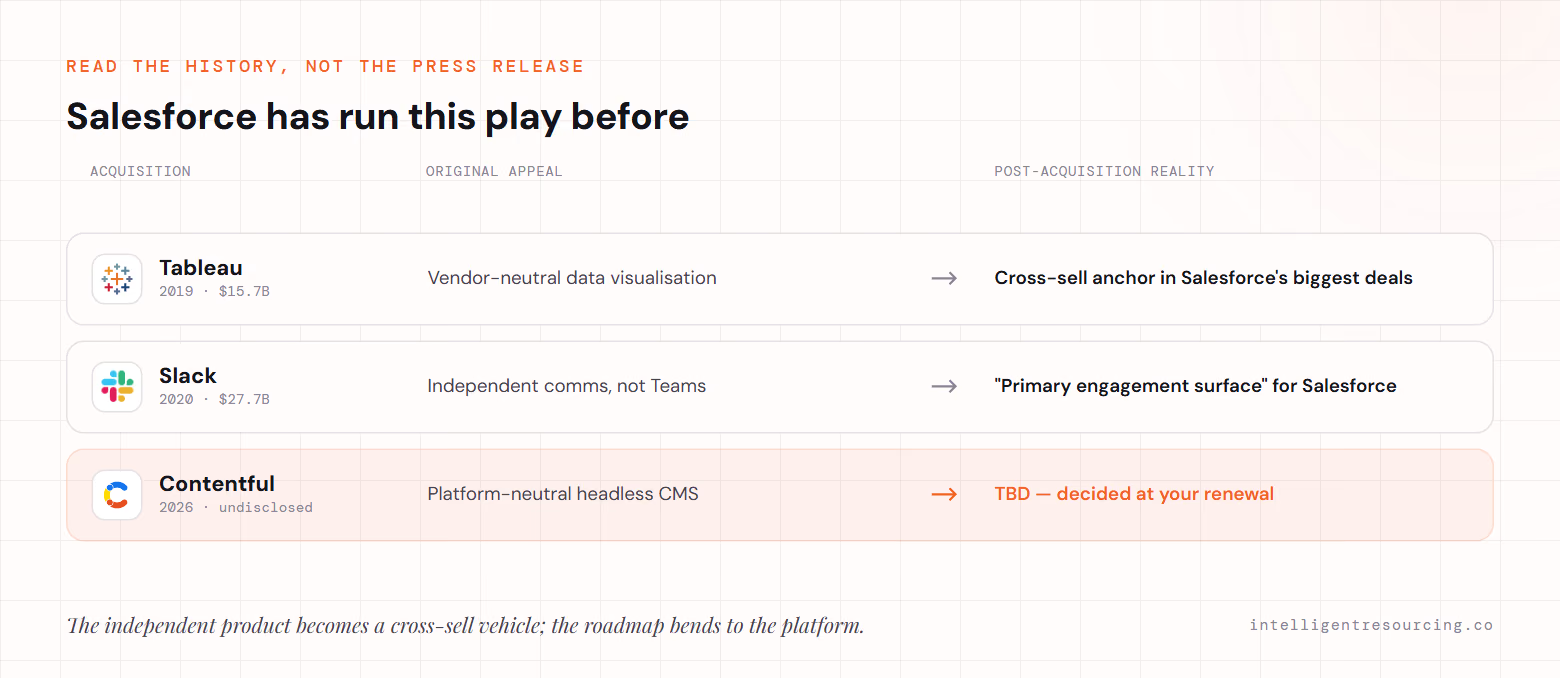

| Acquisition | Year | Price | Original appeal | Post-acquisition reality |

|---|---|---|---|---|

| Tableau | 2019 | $15.7B | Vendor-neutral data visualisation | Cross-sell anchor in Salesforce’s largest enterprise deals |

| Slack | 2020 | $27.7B | Independent comms, not Teams | “Primary engagement surface” for Salesforce products |

| Contentful | 2026 | Undisclosed | Platform-neutral headless CMS | TBD |

Salesforce has been explicit that its goal is to become a one-stop shop for enterprise operations, and every acquisition advances that goal in a predictable way. The independent product becomes a cross-sell vehicle, the developer-first positioning softens, and the pricing adapts to bundle logic rather than standalone competition.

What Changes for Contentful Customers

Contentful’s current standalone pricing is competitive precisely because it exists in an independent market:

- Free tier for small teams and developers

- Lite plan at $300/month

- Premium with unlimited API calls, plus Personalisation, AI Actions, and Studio add-ons

Once Contentful lives inside Customer 360, your licence stops being a standalone purchasing decision and becomes a line item in your Salesforce ELA negotiation. The negotiating power shifts, and it does not shift in your favour.

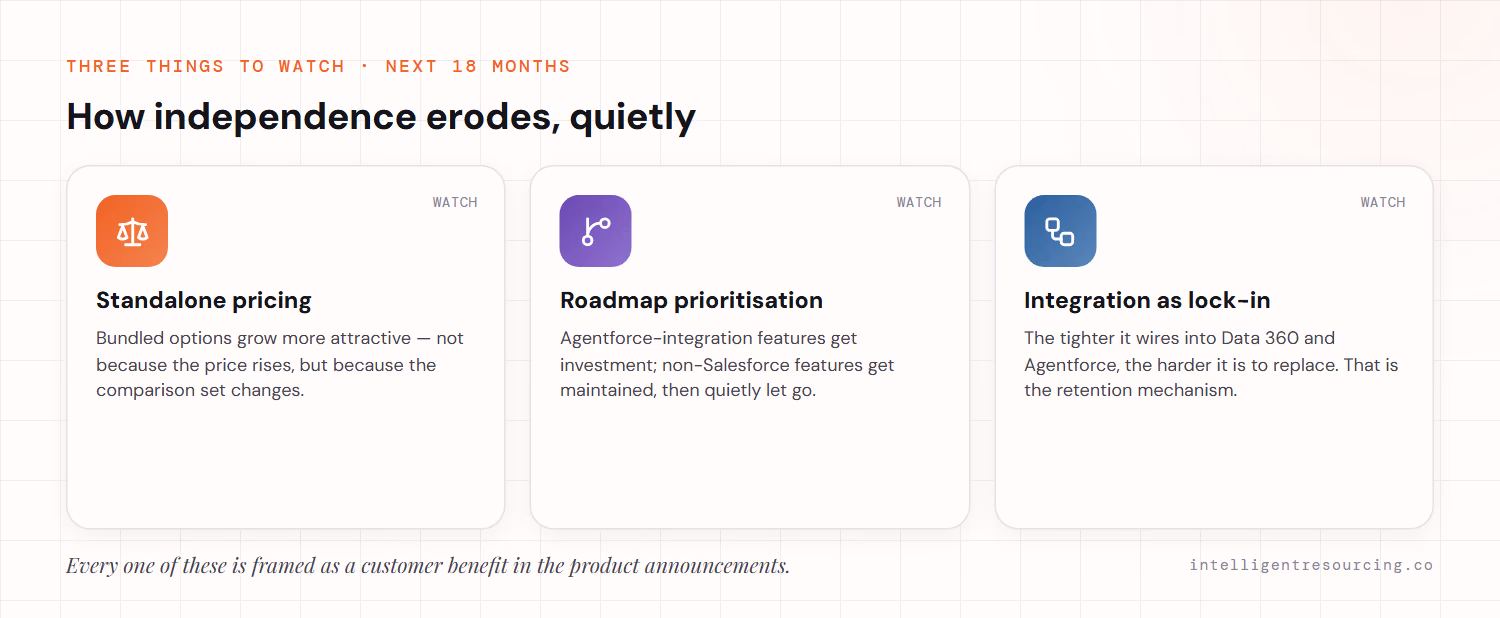

Three things to watch over the next 18 months:

Standalone pricing. Bundled options will become commercially more attractive relative to the standalone plan, not because the price necessarily increases, but because the comparison set changes.

Roadmap prioritisation. Features that deepen Agentforce integration will get investment. Features that serve non-Salesforce customers will get maintained first, then deprioritised, then quietly let go.

Integration depth as lock-in. The tighter Contentful integrates with Data 360 and Agentforce, the harder it becomes to replace. This is the retention mechanism. It is framed as a customer benefit in every product announcement.

What to Do Before the Deal Closes

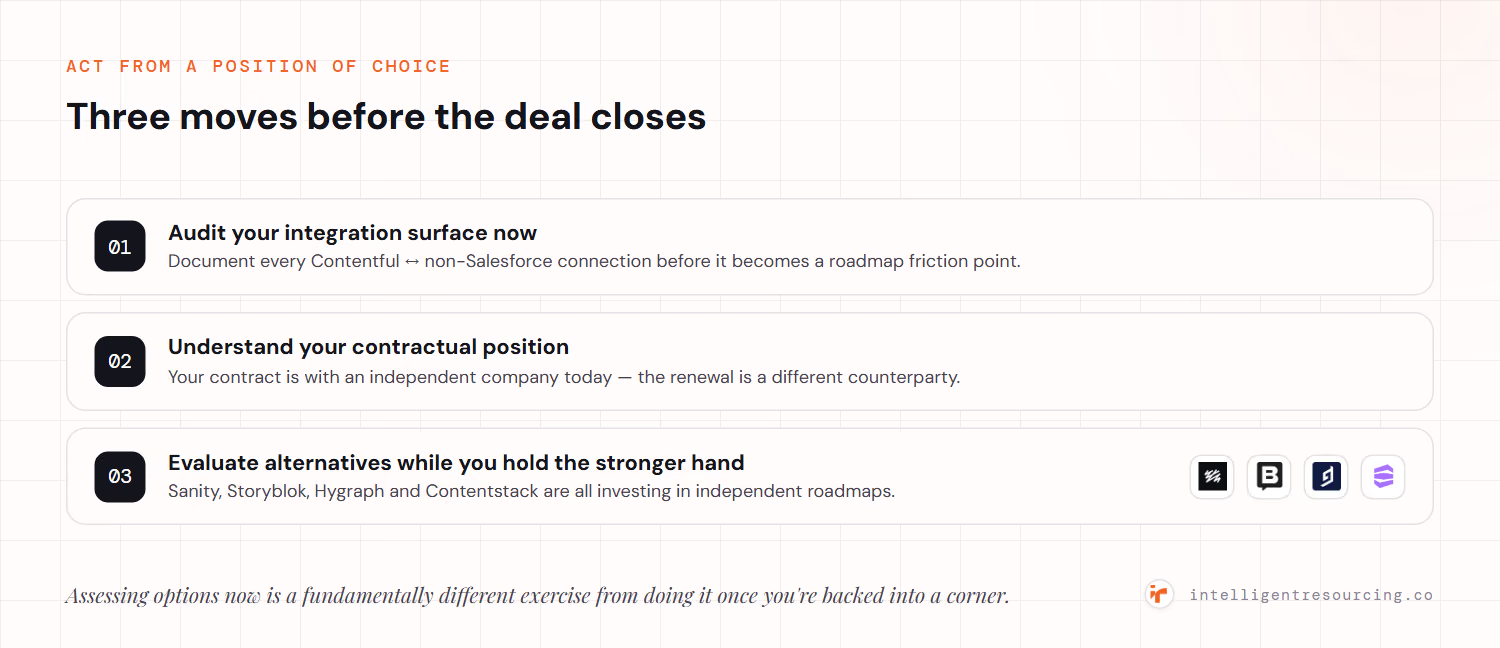

The transaction is expected to close in Salesforce’s fiscal Q3 2027, which gives Contentful customers a window to act from a position of choice rather than necessity. The steps are not complicated, but the timing matters.

Audit your integration surface now. Document every connection between Contentful and your non-Salesforce systems before those connections become friction points in a roadmap that prioritises Salesforce-native paths.

Understand your contractual position. Your current contract exists with an independent company. Acquisitions typically honour existing agreements, but renewals are a different conversation conducted with a different counterparty.

Evaluate alternatives while you still hold the stronger hand. Sanity, Storyblok, Hygraph, and Contentstack are all actively investing in their independent roadmaps. Assessing them now, from a position of choice, is a fundamentally different exercise from doing so after you have been backed into a corner.

The Part Nobody Puts in the Press Release

The headless CMS movement was a direct response to monolithic platform dependency. Enterprises spent a decade ripping apart legacy stacks and rebuilding on composable architecture specifically so they were not beholden to a single vendor’s product decisions. Contentful was one of the primary beneficiaries of that movement, chosen by teams who had already lived through what happens when your CMS vendor’s priorities diverge from yours.

It is now being bought by the largest single-vendor enterprise platform in the world.

The architecture is still sound. API-first content makes sense, Agentforce genuinely benefits from a structured content layer, and the product will likely improve meaningfully in the short term. But the platform neutrality that made Contentful the safe, composable choice is a feature that will erode over time, and the enterprises who understood that independence as a core part of what they were paying for are right to reassess.

The real question is not what the product looks like at close. It is what it looks like at renewal.

RevOps Tools

Intelligent Resourcing builds and runs signal-led GTM systems that keep working no matter which platform gets acquired next.

FAQs

What did Salesforce announce about Contentful?

On 1 June 2026, Salesforce signed a definitive agreement to acquire Contentful, the API-first headless CMS used by more than 4,800 of the world’s leading brands. The transaction is expected to close in Salesforce’s fiscal Q3 2027, subject to customary closing conditions.

Why is Salesforce acquiring Contentful?

Salesforce needed an API-first, composable content engine for its Headless 360 initiative. A native structured content layer also makes Agentforce, its AI agent platform, meaningfully more capable at querying, assembling and delivering content dynamically.

What changes for Contentful customers after the acquisition?

Existing contracts typically continue, but once Contentful sits inside Customer 360 the licence becomes a line item in a Salesforce ELA negotiation. The three things to watch are standalone pricing versus bundles, roadmap prioritisation toward Agentforce integration, and integration depth becoming lock-in.

Should Contentful customers evaluate alternatives now?

Yes, while they can still act from a position of choice before the deal closes. Sanity, Storyblok, Hygraph and Contentstack are all actively investing in independent roadmaps, and assessing them before a renewal is a very different exercise from doing it after.

Will Contentful stay platform-neutral under Salesforce?

The architecture stays API-first, but Salesforce’s history with Tableau and Slack suggests the platform neutrality that made Contentful the safe composable choice will erode over time. The real test is what the product looks like at renewal, not at close.